|

|

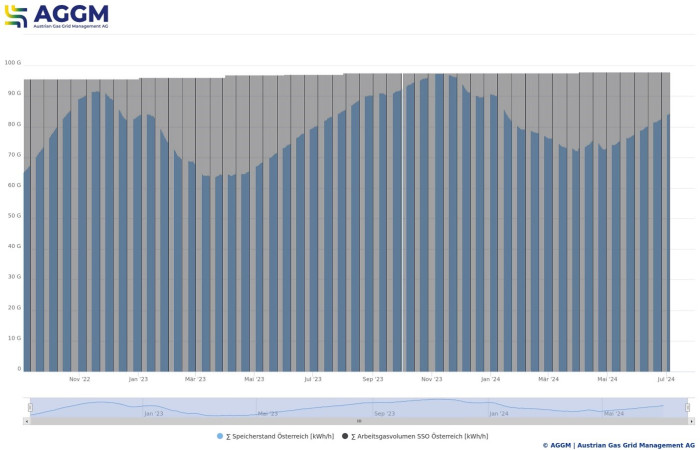

A brief look at the supply situationThe current supply situation and the outlook for the coming winter appear reassuring in view of the high storage levels. With a filling level of more than 84 TWh, the safety cushion for winter 24/25 is considerable.  Source: AGGM, https://platform.aggm.at/portal/visualisation/ts-publication?fav=Qbl However, the end of deliveries via Ukraine is looming at the beginning of 2025, as the transit contract expires at the end of the year. Little is currently known about talks regarding extension options, so the longer-term view beyond winter 24/25 is not quite so reassuring. The shortage of supply would inevitably lead to noticeable price increases. Depending on the scenario, fully and permanently offsetting supplies from Russia could also pose a serious challenge in terms of security of supply. Refilling gas storage facilities from a low level after a cold winter in good time before the following winter period is not possible in all scenarios. Why? Import capacities from Italy and Germany for supplies from alternative sources are limited and their utilisation at a high level is necessary to compensate for supply shortfalls. Only recently was the legal basis created to support the financing of the expansion of import capacities from Germany - keyword WAG loop. However, this additional capacity for imports from alternative sources, which will make a significant contribution to easing the situation, will not be available until 2027. |

|