|

|

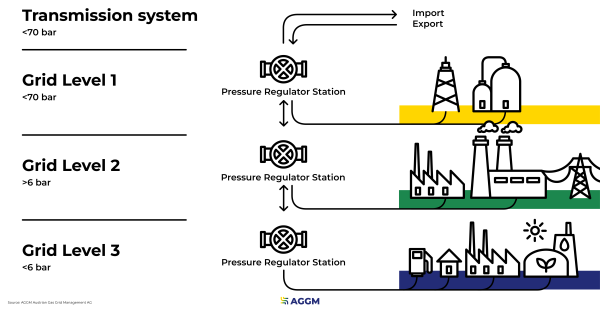

Decommissioning of Gas Networks?The energy system is undergoing transformation. More and more renewable energies - mainly electricity - are feeding into the grid. This has intensified the ongoing debate about the use of gas for space heating. Article 57 of the EU Gas Market Directive 2024/1788 (Directive on common rules for the internal markets for renewable gases, natural gas, and hydrogen) introduces binding requirements for the decommissioning of gas distribution networks for the first time. It obliges gas distribution system operators to draw up decommissioning plans if a foreseeable decline in natural gas demand makes a shutdown necessary. These plans must be reviewed and approved by the relevant national authorities. Only an approved decommissioning plan allows grid operators to reject new connections or terminate existing ones. Certain conditions must be met, such as consultation with consumer organisations and the protection of vulnerable customers or those affected by energy poverty. This regulation is intended to support the transition to renewable energy by enabling an orderly decommissioning of unnecessary gas infrastructure - while avoiding social hardship. It is part of the EU gas and hydrogen market package, which enters into force in July 2024 and governs the gradual phase-out of fossil gas and the ramp-up of the hydrogen market. So much for the specifications from Brussels. In Austria, the EU gas package is mainly to be implemented via an amendment to the Austrian Gas Act (Gaswirtschaftsgesetz). At this point, it is important to note that the directive speaks only of “decommissioning”, never of “dismantling”. By downsizing gas networks, the EU expects both a reduction in greenhouse gas emissions and cost savings in network operation. Complete dismantling of gas pipelines would be the most expensive and complex option for resizing the network. A study by Frontier Economics commissioned by Austria's former Ministry for Climate Protection (BMK) found that dismantling costs in rural areas range between €250,000 and €800,000 per kilometer - costs that can be significantly higher in urban areas due to construction complexity. These figures are based on pipe diameter, expert assessments, and data from ACER. Link: Necessary Framework Conditions for Decommissioning the Gas Distribution Network (German only) Let’s take a closer look at the goals and apply them to the Austrian gas network: Austria’s gas infrastructure is well developed, with more than 46,000 km of pipelines in total. The most powerful gas pipelines are approximately 2,000 km of transmission lines (operated by Gas Connect Austria GmbH and TAG GmbH). These are mainly used for gas transit but also play a key role in import and domestic transport. The distribution network is structured into three grid levels: Grid Level 1: Supra-regional transmission within Austria without customer connections (approx. 1,500 km) Grid Level 2: Supplies to industry and commercial users (approx. 3,600 km) Grid Level 3: Supplies to households and small businesses (approx. 39,500 km)  The most metering points (i.e., end consumer gas withdrawal points) are in Vienna, with about 560,000 metering points. Across Austria, there are 1.2 million network connections, of which approx. 1.1 million are household customers. The Goal: Secure, Cost-Efficient Downsizing We view the aim of creating clear conditions for a secure and efficient downsizing of the gas network - especially on the distribution level - as a positive step. With the removal of the mandatory connection obligation, network operators will no longer be forced to build or maintain inefficient and costly connections. Additionally, there are sections of the network that may become economically unattractive as more households exit gas heating, leading to higher costs for the remaining customers. However, the operating costs of existing pipelines are relatively low and decline only slowly when parts of the network are decommissioned. Therefore, quick cost savings should not be expected in this area. Different considerations apply to reinvestment costs—these can indeed be avoided if infrastructure is decommissioned. Decommissioning of higher grid levels (Transmission pipelines and grid levels 1 and 2) plays a minor role. A high-performance, regional gas grid for methane transport must be maintained in the long term, serving as a collection network for regional biomethane production and the secure coverage of remaining methane demand. The optimal feed-in points can be easily found with inGRID, the feed-in map for renewable gases. If methane volumes decline and the infrastructure is no longer needed for transport, these lines are to be repurposed for hydrogen use, as part of a strategic resizing. Conclusion Decommissioning considerations and the resulting network decommissioning plans, as provided for in Article 57 of the Gas Market Directive, primarily affect those pipeline sections that primarily serve a space heating supply. These essentially concern the local networks that serve the direct grid connection of end customers. According to Article 57, these plans should take into account "the reduced use of natural gas for heating and cooling in buildings where more energy- and cost-efficient alternatives are available." A prerequisite for concrete considerations is the existence of heating and cooling plans in accordance with Article 26 of the Energy Efficiency Directive, which, like the Gas Market Directive, must first be implemented into national law. Despite the foreseeable reduction in gas demand in the space heating sector, it can be assumed that gas customers in this sector will also be in the system in 2040+. Rapid reductions in network costs can be achieved, in particular, by separating infrastructure from the methane regime into a new hydrogen network. |

|